With rare exception, divergences are a key requirement at longer-term inflection points – both tops and bottoms. The most relevant divergences occur across indices, other assets, advance-declines, and momentum. The more powerful the divergences, the greater the likelihood of the significance of the top or bottom.

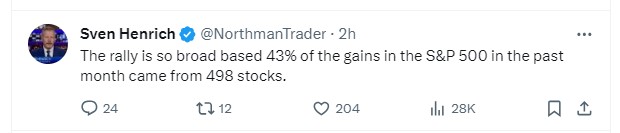

We’re increasingly approaching that type of powerful inflection point. Current divergences may simply portend a reasonably brief and modest correction before more new highs. But this relatively relentless rally since October is getting quite long in the tooth.

The price highs in December were highly unlikely to be “the” price highs for the major indices, simply because momentum was so strong (see my January 8 post with regard to INDU momentum) and nearly all indices and assets were in sync – i.e. the S&P 500, NASDAQ, Russell 2000, 10 year USTs, USD all made relative price highs/lows on December 28.

Fast forward a few weeks to new highs in the S&P 500 and NASDAQ, and how have some of those other assets performed?

· Russell 2000 – down ~4% YTD

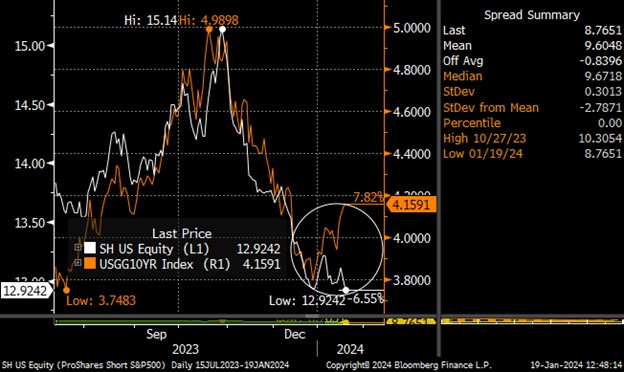

· 10 year UST prices – down ~3% YTD

· NYSE Composite – down ~2% YTD

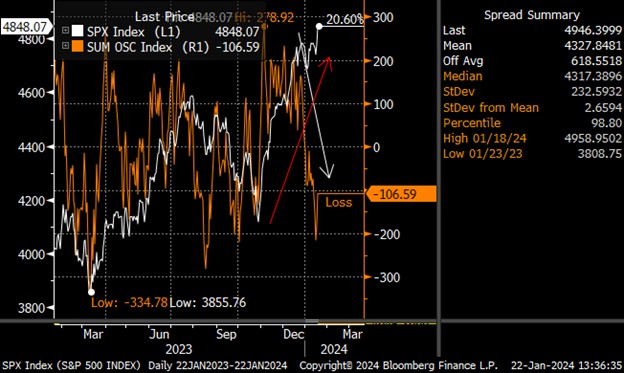

Beyond those cross asset divergences, we’re seeing divergences in volatility (higher lows and higher highs), advance-decline volume, and the McClellan Oscillator… which printed a number below zero on Friday 1/19 when both the S&P 500 and NASDAQ made new highs for the year. Not sure that’s happened before.

And this is all happening while China’s markets (including Hong Kong) are crashing, to the point Chinese authorities are tightening regulations around short selling and considering hundreds of billions of dollars worth of rescue packages for the stock market.

By no means do these divergences ensure prices are going to decline immediately, but it does mean the next correction may not be as simple as “BTFD.” Caution is certainly warranted up here.

Equities

I’ll let the charts do the talking, since in many ways they are self-explanatory. Note the consistency of the momentum (MACD) divergences and the disparate performance across assets.